ZIMBABWE’S life assurance sector has registered robust growth, with the latest figures showing a dramatic 74% surge in insurance revenue during the first half of 2025 compared with the same period in 2024.

The development signals a return to strength in the industry’s core business operations, according to the Insurance and Pensions Commission (IPEC).

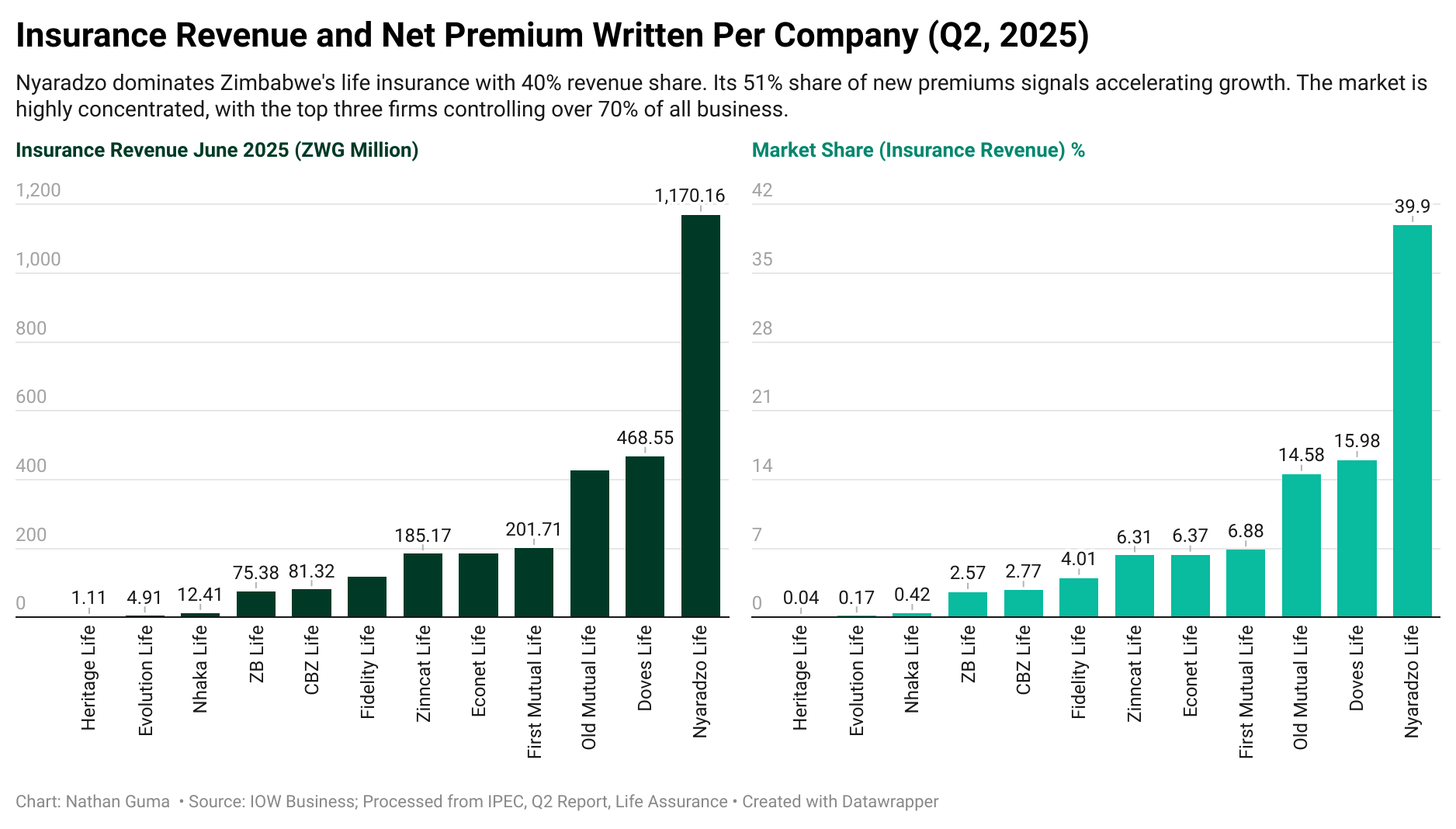

Direct life assurers collectively generated insurance revenue equivalent to US$110.05 million in the six months to 30 June 2025, up markedly from US$63.07 million in the corresponding period of 2024.

This represents a significant rebound for an industry that has previously been reliant on volatile investment income to sustain headline results.

The revenue surge took place against a backdrop of relative macroeconomic stability, underpinned by continued disinflation, a steady exchange rate, and firm foreign currency inflows.

The stabilisation of the broader economic environment provided the sector with firmer ground on which to focus on its primary insurance activities rather than speculative revaluation gains.

Foreign currency business remained a central driver of growth. Transactions in hard currency contributed US$59.21 million to overall revenue, up 38% from US$42.94 million in the same period last year.

In total, foreign currency accounted for 54% of insurance revenue, with recurring business dominating, making up 95% of total revenue and underscoring the stability of income streams.

Crucially, the improvement was rooted in core underwriting. The sector registered a positive insurance service result of ZWG1,133.81 million (equivalent to US$42.55 million), highlighting solid underwriting profitability.

This was supported by a strong average combined ratio of 60.19%, a clear indication that insurers are operating efficiently.

Significantly, all life insurance companies reported combined ratios below 100%, reflecting profitability across the board. CBZ Life, at 99%, was closest to the break-even point, while Fidelity Life recorded the most efficient ratio at 13%.

Financial stability was further reinforced by the sector’s current ratio of 1.07:1, confirming that liquid assets were adequate to meet short-term contractual obligations.

Such indicators demonstrate resilience and prudent balance sheet management during a period of transition.

A notable structural shift in revenue sources was also highlighted in the report. Insurance income is now the dominant contributor, accounting for 81.46% of total revenue.

This marks a sharp departure from 2024, when investment income dominated at 78%.

IPEC attributed this transition to the stabilisation of the exchange rate, which sharply reduced reliance on revaluation gains and fair value adjustments.

The sector’s asset base also reflected this renewed stability, with total assets for direct life insurers increasing by 1.0% to US$590.01 million equivalent (ZWG15.90 billion) by June 2025.

Life reassurers recorded even stronger growth, with assets rising 48% to US$15.17 million equivalent (ZWG408.76 million). Growth drivers included new acquisitions, revaluation gains, and the entry of WAICA Re as a new market participant.

Regulatory compliance remained high as ten of the twelve direct life assurance companies met the US$2 million indexed Minimum Capital Requirement (MCR).

The life reassurance sector performed particularly strongly, with an average prescribed assets compliance ratio of 26.31%, comfortably exceeding the statutory minimum of 15%. – IOW Business.